![]()

[Mar 15, 2026] Updates Up to 365 days On Valid ClaimCenter-Business-Analysts Braindumps

Best QualityClaimCenter-Business-Analysts Exam Questions Guidewire Test To Gain Brilliante Result

NEW QUESTION # 10

A catastrophe has been created in ClaimCenter for Tropic Storm Dorian. Succeed Insurance requires that all claims resulting from the storm be attributed to that catastrophe when they are entered in ClaimCenter. The completion target is within three (3) days of claim creation and should be escalated if it is not completed within five (5) days.

Which required element for a business activity rule is missing?

- A. RuleCondition

- B. Actions

- C. AppliesTo

- D. TriggerEntity

Answer: B

Explanation:

A complete Business Rule (specifically one designed to generate an Activity) consists of a Context (Trigger

/Entity), a Condition (Logic), and an Action (Execution).

* Missing Element: Actions (Option A):The scenario describes thetrigger("when they are entered"), the intent/condition("resulting from the storm"), and theparametersof the resulting activity (Target: 3 days, Escalation: 5 days). However, it fails to specify theActiondetails required to execute the rule:

specifically,whothe activity should be assigned to (The Assignee) and the specific instruction tocreate the activity instance. Without defining the Action (e.g., "Create Activity 'Review Catastrophe' and Assign to Claim Owner"), the rule cannot function.

* Why other options are present:

* TriggerEntity (B):Implied as the Claim (since the text says "whenthey[claims] are entered").

* RuleCondition (C):While "resulting from the storm" is vague, it represents the business condition. TheAction(assignment) is the most glaring omission preventing the workflow from reaching a user.

* AppliesTo (D):This generally refers to the root entity (Claim), which is identified.

NEW QUESTION # 11

A claim for an auto accident in California has been assigned to an insurance Adjuster in the Midwest region for investigation and processing. The claim has been flagged as "Low Complexity" in ClaimCenter. The Adjuster has an authority limit for total reserves of $30,000 and has created reserves totaling $35,000.

What is the correct approval routing for this transaction?

- A. The transaction will require approval from another team member who has the authority limit to approve.

- B. This transaction will not require approval because the claim is identified as low complexity.

- C. This transaction will require approval because the Adjuster does not work in the same region where the claim was reported.

- D. The transaction will require approval from the Supervisor of the group.

Answer: D

Explanation:

Based on theGuidewire ClaimCenter Financials and Authority Limitsdocumentation, the correct behavior for this scenario is determined by the strict enforcement ofAuthority Limits, regardless of claim complexity or geographic region.

In ClaimCenter, every user is assigned specific authority limits for various financial transactions, including reserves, payments, and recovery reserves. These limits are absolute constraints designed to control financial exposure. In the scenario provided, the Adjuster attempted to set a reserve of$35,000, which exceeds their authorized limit of$30,000.

When a user submits a financial transaction that exceeds their pre-configured authority limit, ClaimCenter automatically triggers anApproval Workflow. The system validates the transaction amount against the user's limit at the time of submission. Since the limit is breached, the transaction is not committed immediately to the database as "Submitted"; instead, it enters a"Pending Approval"status.

Routing Logic:

The standard, out-of-the-box approval routing logic in ClaimCenter follows the Group Hierarchy.

* The system identifies the group to which the Adjuster belongs.

* It creates anApproval Activity.

* This activity is assigned to theSupervisorof that group.

The Supervisor must then review the transaction. If the Supervisor has sufficient authority (greater than

$35,000), they can approve it. If the Supervisor also lacks sufficient authority, they must still "approve" it to escalate the request further up the hierarchy totheirmanager, until it reaches a user with sufficient limits.

Why other options are incorrect:

* A (Complexity):Claim complexity flags (e.g., "Low Complexity") are often used forAssignmentrules (Segment-based assignment) or straight-through processing ofdocuments, but they do not override Financial Authoritycontrols. A low-complexity claim still requires financial oversight if the dollar amount is high.

* B (Peer Approval):Approval routing is hierarchical, not peer-to-peer. It does not look for "any" team member; it looks specifically for the defined Supervisor.

* C (Region):The region mismatch might trigger an assignment rule or a validation warning depending on configuration, but the specific trigger for theapprovalhere is purely the financial discrepancy ($35k

> $30k), not the geography.

NEW QUESTION # 12

Succeed Insurance has a strategic initiative to change auto insurance into a pay-as-you-drive model... When claims are processed, claimants must provide the log from the application for the date of incident. The log's details are essential to validation and analysis of the monitoring system's activity at the time of the incident.

Without the application log, claims should not be processed to indemnification.

Executives say the implementation team must maintain the base product functionality where appropriate and only change those things essential to the success of the initiative...

Which two requirements are in scope based on the guiding principles? (Choose two.)

- A. As an Adjuster, vehicle mileage/kilometers must be captured during adjudication to track mileage

/kilometers, and potentially prevent fraudulent activities. - B. As a business, integration to the top five vehicle manufactures must be completed to maximize accuracy of claim processing. Succeed intends to complete one integration every 30 days.

- C. As an Adjuster, the insured application log must be received, reviewed, and attached to the claim to analyze and validate the monitoring systems activity at the time of the claim.

- D. As an Adjuster, the system should prevent indemnification of claimants if the application log has not been provided and reviewed to prevent payments without validation.

Answer: C,D

Explanation:

When defining scope based on specific strategic initiatives and guiding principles (such as "only change those things essential"), the Business Analyst must map requirements directly to the stated business rules and critical success factors.

* Requirement D (Log Intake):The scenario explicitly states:"The log's details are essential to validation and analysis... claimants must provide the log."Option D directly captures this by requiring the log to be received, reviewed, and attached. This is the core data intake requirement.

* Requirement C (Validation Rule):The scenario states:"Without the application log, claims should not be processed to indemnification."Option C directly maps to this business rule. It utilizes base product capabilities (Validation Rules) to enforce the "No Log, No Pay" constraint, ensuring the initiative's security and validity.

Why other options are incorrect:

* Option B (OEM Integration):The scenario mentions leveraging integration "where possible," but creates a requirement for "application logs," not direct integration with "top five vehicle manufacturers." Adding a rigid schedule ("one integration every 30 days") is a high-cost, high- complexity constraint that contradicts the principle of maintaining base functionality and minimizing cost/maintenance unless explicitly required.

* Option A (Mileage):While mileage is part of the concept, theessentialrequirement described for the claim process is thevalidation of the logfor the incident. Tracking mileage is secondary to the critical path of validating the accident data via the log.

NEW QUESTION # 13

When creating a new Personal Auto claim, Succeed Insurance would like to identify when Rideshare is the primary use for a vehicle. A Business Analyst (BA) thinks that Primary Use already exists as a typekey on the Vehicle Details screen.

What are two ways the BA can confirm whether this field is configured in ClaimCenter and, if it is, which values are available in the typelist? (Choose two.)

- A. Access the Data Dictionary > Click the Data Entities link > Open the PrimaryUse entity from left-hand pane to view field details on the right pane.

- B. Access the Guidewire ClaimCenter Application Guide > Go to section on Personal Auto Object Model which lists available entities.

- C. Log in to ClaimCenter > Create a new Personal Auto claim > Navigate to Vehicle Details > Use keyboard shortcut CTRL + F to find information about the fields on the screen.

- D. Open Guidewire Studio for ClaimCenter > Navigate to the Vehicle Details screen > Locate the Primary Use field to view its typelist.

Answer: A,D

Explanation:

To verify the configuration of a specific field and its available values (typelist) within a specific implementation (like Succeed Insurance), a Business Analyst must consult the sources that reflect the current, actual system configuration, not just the out-of-the-box documentation.

* Option A (Data Dictionary):TheData Dictionaryis the definitive, generated documentation of the running application's data model. It lists allEntities(such as Vehicle) and theirTypekeys(such as PrimaryUse). By navigating to the Data Dictionary, a BA can confirm if the field exists in the database schema and view the specificTypelistvalues (e.g., "Rideshare", "Commuting", "Pleasure") associated with it. This is a primary tool for BAs to understand the data structure.

* Option D (Guidewire Studio):Guidewire Studiois the Integrated Development Environment (IDE) used to configure the application. It contains the "Source of Truth" for all configuration files. A BA (or a developer assisting them) can open thePage Configuration (PCF)files to see the Vehicle Details screen definition or open theTypelistfiles (.tti/.ttx) directly to see exactly which values are defined and active.

Why other options are incorrect:

* Option B (Application Guide):The Application Guide documents theBase (Out-of-the-Box)product features. It does not contain customer-specific customizations or extensions. If "Primary Use" or

"Rideshare" were added or modified by Succeed Insurance, the Application Guide would not reflect this.

* Option C (UI Inspection with CTRL+F):While logging into the application allows a user to see the dropdown on the screen, the shortcutCTRL + Fis merely the browser's "Find" function. It searches visible text on the page but does not provide configuration metadata, hidden values, or definitive proof of the underlying data model structure. The correct shortcut for inspecting widget properties in Guidewire is Alt + Shift + I (Location Info), but even that is less efficient for viewing a full typelist than the Data Dictionary or Studio.

NEW QUESTION # 14

What two pieces of information enable the Business Analyst (BA) to trace back to the root cause of an issue?

(Choose two.)

- A. The change history on the Document Control tab of the Adjudicate - Create and Maintain Exposures for Vehicle User Story Card

- B. The caution points indicated on the User Story Workflow

- C. The unique Story Card number associated with the acceptance criteria

- D. The unique requirement numbers related to User Story

- E. The Approver Notes on the Acceptance tab of the Adjudicate - Create and Maintain Exposures for Vehicle User Story Card

Answer: C,D

Explanation:

In Guidewire implementation methodology (Agile/SurePath), Traceability is maintained through specific unique identifiers that link the code and test cases back to the business definition.

* Unique Requirement Numbers (Option E):Every granular business requirement is assigned a unique ID (e.g., CC-FNOL-001). If a defect or issue arises during testing or production, the BA uses this number to find the exact text of the requirement that was implemented. This helps determine if the issue is a "bug" (code doesn't match requirement) or a "gap" (requirement was missing or wrong).

* Unique Story Card Number (Option A):User Stories act as containers for requirements. The Story Card Number (e.g., Story-105) links the individual requirements to the broader feature context. Tracing back to the Story Card allows the BA to review the original scope, the UI mockups, and the Acceptance Criteria associated with that feature to understand the "Root Cause" of the misunderstanding or failure.

Why other options are incorrect:

* Option B (Caution points):These are process diagrams notes, useful for training but not for system traceability.

* Option C (Change History):While useful for seeingwhoedited a document, it does not provide the structural link between a system error and the business definition like the IDs do.

* Option D (Approver Notes):These confirm sign-off but rarely contain the functional detail needed to diagnose a root cause.

NEW QUESTION # 15

Which two best practices should a Business Analyst (BA) follow to be prepared for a Requirements Workshop? (Choose two.)

- A. Ask the Project Manager to set an agenda.

- B. Review notes from Inception Workshop.

- C. Review acceptance criteria.

- D. Invite end users with knowledge of related process.

- E. Review base product functionality of ClaimCenter for related process.

Answer: B,E

Explanation:

Preparation is key to a successful Requirements Workshop (or Elaboration Workshop). The BA must enter the room with a clear understanding of the project scope and the tool's capabilities.

* Review Notes from Inception (B):TheInception Phasedefines the high-level scope, vision, and business objectives. Reviewing these notes ensures the BA understands the boundaries of the discussion (e.g., "We are doing Auto Hail damage, but not Property Hail damage yet") and the strategic goals defined by the sponsors.

* Review Base Product Functionality (C):To effectively lead the session and recommend solutions (as seen in Question 22), the BA must be familiar with how ClaimCenter handles the specific topic (e.g., Check Wizards, Coverage Verification) out-of-the-box. This allows the BA to demo standard features during the workshop to drive "Fit-to-Standard" discussions rather than starting from a blank sheet of paper.

* Why not A, D, or E?Inviting users (A) and setting agendas (E) are logistical tasks often handled by the Project Manager or shared; they are not "personal preparation" of knowledge. Acceptance Criteria (D) are typically writtenduringorafterthe workshop, not reviewed beforehand (unless refining an existing story).

NEW QUESTION # 16

Which two components are necessary to create the check(s) using the wizard? (Choose two.)

- A. Payment tied to a reserve line

- B. Payment tied to an activity

- C. Date of the claim

- D. Payee

Answer: A,D

Explanation:

The Check Wizard in Guidewire ClaimCenter enforces strict financial integrity rules. To successfully create a check, the user must define the source of funds and the recipient.

* Payment tied to a Reserve Line (Option A):Every payment must be allocated to a specificReserve Line(combination of Exposure, Cost Type, and Cost Category). This ensures that the payment consumes the correct financial reserves and maps to the correct coverage on the policy. You cannot create a "floating" payment; it must be tied to a reserve line.

* Payee (Option C):A check is a legal instrument that must be payable to a specific entity. Selecting a Payee(from the claim contacts) is a mandatory step in the wizard.

Why other options are incorrect:

* B (Activity):While paymentscanbe linked to activities (e.g., Service Requests), it is optional. Most indemnity payments are made directly without an underlying activity.

* D (Date of claim):The Loss Date is a property of the claim, but it is not a component selected or created duringthe check wizard process. The relevant dates in the wizard are the "Service Period" or

"Scheduled Send Date."

NEW QUESTION # 17

An auto claim is owned by Adjuster1. The Customer Service Representative (CSR) that created the claim owns one follow-up activity on the claim. An Injury Specialist owns an injury exposure on the claim. All these persons are members of Auto Team 1.

The Team Lead determines that Adjuster1 is overworked and reassigns the claim to Adjuster2, a member of Auto Team 2.

Which three people now have access to the claim? (Choose three.)

- A. Adjuster2

- B. Adjuster1

- C. CSR

- D. The Claimant

- E. Injury Specialist

- F. Special Investigations Unit

Answer: A,C,E

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In Guidewire ClaimCenter, access to a claim file is determined by Access Control Lists (ACLs), which are dynamically updated based on user roles and ownership. A user is granted access to a claim if they own the claim itself, or if they own a sub-object within that claim, such as an Activity or an Exposure.

* Adjuster2 (Option E):Upon reassignment, Adjuster2 becomes the newClaim Owner. The owner of the claim record always has full view and edit access to the claim.

* CSR (Option C):The CSR retains ownership of a specificActivity(the follow-up task). In the ClaimCenter security model, owning an open activity on a claim grants the user "view" access to the parent claim so they can perform the necessary work to complete their task. Reassigning the claim header does not automatically reassign the activities owned by other users.

* Injury Specialist (Option D):This user owns anExposure(a distinct financial sub-record for a specific coverage feature). Similar to activities, owning an exposure grants access to the parent claim. The reassignment of the main claim file from Adjuster1 to Adjuster2 does not strip the Injury Specialist of their ownership of the specific injury exposure.

Why Adjuster1 loses access:Adjuster1 was the previous owner. Once ownership is transferred to Adjuster2 (who is in a different group, "Auto Team 2"), Adjuster1 no longer meets the criteria for ownership access.

Unless Adjuster1 is explicitly added to the ACL manually or has "Super User" privileges (not stated), they lose the automatic access rights associated with being the owner.

NEW QUESTION # 18

An Adjuster at Succeed Insurance increases the reserve on a claim's exposure from $1,000 to $1,500 to account for inflation in repair costs. A week later, a Supervisor reviews the claim and wants to know specifically who made this change, the exact date and time it was made, and what the previous value was.

The Supervisor needs a chronological audit trail of changes to the claim file without navigating through complex financial ledgers.

Which screen in the ClaimCenter user interface should the Supervisor access to find this information?

- A. Loss Details > Status

- B. Notes

- C. History

- D. Financials > Transactions

Answer: C

Explanation:

In Guidewire ClaimCenter, the History screen serves as the automated audit trail for the claim file. It is designed to capture and display a chronological list of significant events and user actions that have occurred throughout the claim's lifecycle.

* Audit Trail Functionality:The History screen automatically records specific types of events, including:

* Field Changes:When critical fields (like Reserve Amounts) are modified, the system logs the

"Old Value" and the "New Value."

* Assignment Changes:Tracks when the claim was transferred from one user to another.

* Rule Execution:Logs when specific business rules (like "Exception Flagged") are triggered.

* Data Points:For each entry, the History screen displays theUserwho performed the action, the Timestampof the event, and aDescriptionof the change.

Why other options are incorrect:

* Financials > Transactions (A):While this screen shows the financial T-account entries (debits/credits) for the reserve increase, its primary purpose is accounting analysis. It is less efficient for a supervisor looking for a simple "Who/When/What" audit trail compared to the History screen.

* Notes (C):Notes are typically used for qualitative narratives and manual entry. While a system notecan be generated for a reserve change, the History screen is the dedicated, non-editable system of record for tracking field changes.

* Loss Details > Status (D):This screen shows thecurrentstate of the claim (e.g., Open, Closed, Litigation Status) but does not provide a historical log of previous values or the specific user actions that led to the current state.

NEW QUESTION # 19

Succeed Insurance has a requirement to add a new high-risk indicator to the Claim Status screen for property claims that have a lien on the property. A new icon will be added to the configuration to provide a visual indicator making it easier for Adjusters and other ClaimCenter users to determine that a claim has a lien.

Which two common areas of the user interface (UI) can display the new lien icon? (Choose two.)

- A. Sidebar

- B. Info Bar

- C. Screen Area

- D. Tab Bar

- E. Workspace

Answer: B,C

Explanation:

In the standard Guidewire ClaimCenter User Interface architecture, high-priority alerts and claim indicators are displayed in two primary locations to ensure visibility:

* The Info Bar (Option D):This is the persistent strip located at the top of the claim file (just below the Tab Bar). It remains visible regardless of which specific claim sub-screen (Medical, Financials, Notes) the user is navigating. It is designed specifically to host "High Risk Indicators" such as Litigation, Fatalities, Coverage issues, and in this scenario, a "Lien" indicator. This ensures the adjuster is aware of the critical status immediately upon opening the claim.

* The Screen Area (Option A):Specifically, theClaim Status(or Summary) screen-which resides in the main Screen Area-contains a dedicated section for "Claim Indicators." Here, the icon is displayed along with a text description and potential toggle status (On/Off). The prompt explicitly mentions the requirement to "add a new high-risk indicator to the Claim Status screen," confirming the Screen Area as the second location.

Why other options are incorrect:

* Sidebar (B):The sidebar (left panel) is used for the "Actions" menu and navigation links (steps) to move between screens. It does not typically host status icons for the claim object itself.

* Workspace (C):While "Workspace" can refer to the application frame, in UI terminology, it often refers to the specific worksheets (bottom pane) or the container, not the specific UI element for indicators.

* Tab Bar (E):The Tab Bar is for high-level navigation (Claim, Desktop, Administration, Search) and does not display claim-specific data icons.

NEW QUESTION # 20

Which scenario shows a Business Analyst (BA) demonstrating an important way to use Guidewire's Business Process Flows during a product implementation?

- A. We will be leveraging base configuration, so we will reference Guidewire's Business Process Flow for assignments to make changes to our business process for claim assignment.

- B. We will use our Business Process Flow for First Notice of Loss (FNOL) to guide the development of custom configuration instead of Guidewire's Process for Flow FNOL because we would like to continue using our current process.

- C. We will not reference Guidewire Business Process Flows because we do not have the process flows for our current process documented to compare it.

- D. We will compare our Business Process Flow for First Notice of Loss (FNOL) to Guidewire's Business Process Flow for Reserve entry to identify whether process gaps exist.

Answer: A

Explanation:

One of the primary value drivers of a Guidewire implementation is the "Adopt" or "Fit-to-Standard" approach, which encourages insurers to align their operations with industry best practices embedded in the software.

* Best Practice (Option B):The most effective use of Guidewire's standard Business Process Flows is to use them as a reference tochange the customer's internal processes. Instead of customizing the software to match a legacy (and potentially inefficient) way of doing things, the BA uses the base product flow to demonstrate how the system works out-of-the-box and guides the business to adapt their assignment logic to match this standard. This reduces customization costs and simplifies future upgrades.

* Why Option A is incorrect:This describes the "Gap" approach where the software is heavily customized to fit the old process ("continue using our current process"). This is considered an anti- pattern in modern implementations as it increases technical debt.

* Why Option C is incorrect:Comparing FNOL (intake) to Reserves (financials) is comparing two completely different lifecycle stages, making the gap analysis invalid.

* Why Option D is incorrect:Lack of documentation is not a valid reason to ignore the standard flows; in fact, the standard flows can serve as thenewdocumentation for the undocumented process.

Based on the Guidewire ClaimCenter Business Analyst documentation and the provided exhibits, here is the verified answer for Question 42.

NEW QUESTION # 21

During claim intake and adjudication, Adjusters capture contact information for the insured and all claimants.

To improve customer service and reduce the time required to reach these contacts to gather additional claim information, Succeed Insurance will capture the preferred contact method for all person contacts. The new field will be added to the contact details screen of the user interface (UI) as a drop-down list displaying all valid contact methods including email, mail, and phone.

Which version correctly lists the preferred contact methods in the Typelists tab of the Parties Involved User Story Card?

- A. Option A

- B. Option B

- C. Option D

- D. Option C

Answer: B

Explanation:

To correctly document a Typelist in a User Story Card, the Business Analyst must understand both the data structure (Codes vs. Names) and the configuration state (New vs. Modified).

* Code Validity:In Guidewire, aTypecode(the value stored in the database) must be a unique identifier for each option in the list.

* Option Bcorrectly lists distinct codes: email, mail, and phone.

* Options A and Care incorrect because they list theTypelist Name(PreferredContactMethod) as the Codefor every single row. You cannot have multiple entries with the same primary key (Code) in one list.

* Configuration State (New vs. Modified):The PreferredContactMethod typelist is a standardBase Productfeature in Guidewire ClaimCenter. It already exists out-of-the-box.

* Option Bcorrectly identifies the Status as"Modified". When you add values to or configure an existing base typelist, you document it as "Modified".

* Option Dis incorrect because it lists the Status as"New". This would imply creating a brand new custom typelist (e.g., MyCustomList_Ext), which is not necessary for standard contact methods.

Therefore,Option Bis the only version that has valid, unique codes and the correct configuration status.

NEW QUESTION # 22

An Adjuster at Succeed Insurance creates a check with a partial payment of $1,200 for medical expenses payable to a claimant who was injured in a collision. The check has completed the following processing steps:

. The payment exceeded the Adjuster's authority limits, changing the status to Pending Approval.

. The Adjuster's supervisor reviewed and approved the payment, changing the status to Awaiting Submission.

. A batch process sent the check to the external check processing system, changing the status to Requested when ClaimCenter received an update from the external system.

The Adjuster received new information indicating that the check amount should be reduced to $950.

Which action should the Adjuster take?

- A. Void the check and create a new check for the correct amount.

- B. Edit the check and change the amount, then submit it for processing.

- C. Ask the bank to hold the check and create a new check for the correct amount.

- D. Stop the check and create a new check for the correct amount.

Answer: A

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In the lifecycle of a check within Guidewire ClaimCenter, the Requested status indicates that the payment instruction has been successfully handed off to the downstream check writing or electronic funds transfer system. Once a check reaches this status, it is considered a committed financial transaction and is locked from further editing.

* Why Option A is incorrect:You cannot edit a check that is in "Requested" status. The "Edit" button will likely be disabled or the fields locked because the data has already left the system.

* Why Option C is incorrect:A "Stop" payment is typically reserved for scenarios where a physical check has been lost, stolen, or destroyedafterit was printed and mailed. While a Stop Payment does prevent the check from being cashed, it is a specific banking process often involving fees.

* Why Option D is Correct:To correct an administrative error (such as the wrong amount) for a check that has been processed but not yet negotiated (cashed), the standard procedure is toVoidthe check.

Voiding the check in ClaimCenter performs two critical functions:

* It reverses the financial T-accounts (reserves and payments) associated with the transaction, ensuring the claim financials are accurate.

* It updates the status to "Voided," effectively cancelling the payment in the system.

After voiding the incorrect check ($1,200), the Adjuster must then create anew checkfor the correct amount ($950) to pay the claimant.

NEW QUESTION # 23

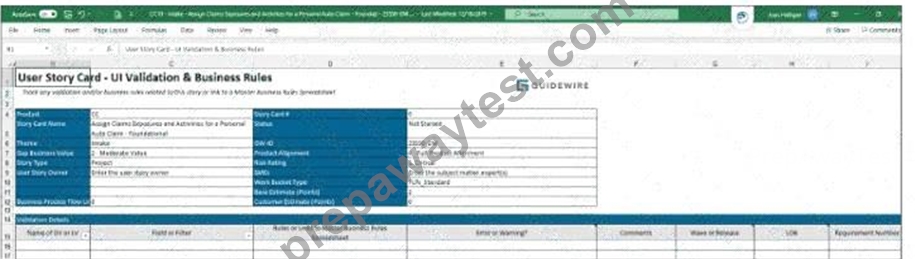

At Succeed Insurance, new personal auto claims involving a fatality are assigned to a High Complexity Auto group made up of Adjusters with at least eight years of experience dealing with the issues and emotions commonly found in claims involving fatalities. Fatality claims typically take 18 to 24 days to complete. The assigned Business Analyst (BA) will document the assignment rule for this requirement in User Story Card Assign Claims Exposures and Activities for a Personal Auto Claim - Foundational. The existing tab UI Validation & Business Rules shown below is not a good fit for assignment rules, so a new tab will be added to the Story Card.

Which two sets of columns should the new tab include to accurately capture the assignment rule requirements? (Choose two.)

- A. Global Assignment Rule, Default Group Assignment Rule, Exit Type

- B. Name of DV or LV, Field or Filter, Rules or Links to Master Business Rules Spreadsheet

- C. Error or Warning?, Base Product/New/Modified, Acceptance Criteria

- D. Entity, Line of Business, Rule Conditions, Rule Actions

- E. Comments, Wave or Release, Requirement Number

Answer: D,E

Explanation:

When documenting Assignment Rules (or any business logic) in a User Story Card or a separate Business Rules spreadsheet, the Business Analyst must capture specific metadata that allows developers to implement the logic correctly in Gosu (Guidewire's programming language).

* Option D (Entity, Line of Business, Rule Conditions, Rule Actions):This is the core logical definition of the rule.

* Entity:Defines what object is being assigned (e.g., Claim, Exposure, Activity).

* Line of Business:Specifies the scope (e.g., Personal Auto).

* Rule Conditions:Captures the "IF" logic (e.g., "IF Loss Cause = Fatality AND LOB = Personal Auto").

* Rule Actions:Captures the "THEN" logic (e.g., "THEN Assign to Group: High Complexity Auto").

* This structure mimics the actual implementation pattern in Guidewire Studio (Rule Sets).

* Option E (Comments, Wave or Release, Requirement Number):These are standard project management and traceability columns required foranyrequirements artifact.

* Requirement Number:Links the specific rule row back to the high-level business requirement.

* Wave or Release:Indicates when this specific rule needs to be deployed.

* Comments:Provides context or clarification for the developer.

Why other options are incorrect:

* Option A:These columns ("Name of DV or LV", "Field or Filter") are specific toUI Validation(the tab currently shown in the image). They describe screen widgets and validation errors, not backend assignment logic.

* Option B:While "Global Assignment Rule" and "Default Group Assignment Rule" are valid Guidewire concepts, listing them ascolumnsis not the standard way to document a list of requirements. Usually, the ruletypewould be a single column, but "Exit Type" is a technical implementation detail (part of the rule set execution) rather than a business requirement column.

* Option C:"Error or Warning?" is specific to Validation Rules (stopping a user from proceeding), not Assignment Rules (routing a work item).

Next Step:Would you like me to generate a sample "Assignment Rule" table structure that shows exactly how this Fatality claim rule would be entered into the columns described in Option D?

NEW QUESTION # 24

Succeed Insurance has a requirement to add a new high-risk indicator to the Claim Status screen for property claims that have a lien on the property. A new icon will be added to the configuration to provide a visual indicator making it easier for Adjusters and other ClaimCenter users to determine that a claim has a lien.

Which two common areas of the user interface (UI) can display the new lien icon? (Choose two.)

- A. Sidebar

- B. Info Bar

- C. Screen Area

- D. Tab Bar

- E. Workspace

Answer: B,C

Explanation:

In the standard Guidewire ClaimCenter User Interface architecture, high-priority alerts and claim indicators are displayed in two primary locations to ensure visibility:

* The Info Bar (Option D):This is the persistent strip located at the top of the claim file (just below the Tab Bar). It remains visible regardless of which specific claim sub-screen (Medical, Financials, Notes) the user is navigating. It is designed specifically to host "High Risk Indicators" such as Litigation, Fatalities, Coverage issues, and in this scenario, a "Lien" indicator. This ensures the adjuster is aware of the critical status immediately upon opening the claim.

* The Screen Area (Option A):Specifically, theClaim Status(or Summary) screen-which resides in the main Screen Area-contains a dedicated section for "Claim Indicators." Here, the icon is displayed along with a text description and potential toggle status (On/Off). The prompt explicitly mentions the requirement to "add a new high-risk indicator to the Claim Status screen," confirming the Screen Area as the second location.

Why other options are incorrect:

* Sidebar (B):The sidebar (left panel) is used for the "Actions" menu and navigation links (steps) to move between screens. It does not typically host status icons for the claim object itself.

* Workspace (C):While "Workspace" can refer to the application frame, in UI terminology, it often refers to the specific worksheets (bottom pane) or the container, not the specific UI element for indicators.

* Tab Bar (E):The Tab Bar is for high-level navigation (Claim, Desktop, Administration, Search) and does not display claim-specific data icons.

NEW QUESTION # 25

......

Focus on ClaimCenter-Business-Analysts All-in-One Exam Guide For Quick Preparation: https://www.prepawaytest.com/Guidewire/ClaimCenter-Business-Analysts-practice-exam-dumps.html

Tested Material Used To ClaimCenter-Business-Analysts: https://drive.google.com/open?id=1295JYCkMx6vNq-3grixYbZXa8a9WBhJn